Navigating the Future: Supply Chain, Digitalization and Consumer Behavior in the FMCG Industry in North Macedonia

- Home Main

- Case Studies

- Navigating the Future: Supply Chain, Digitalization and Consumer Behavior in the FMCG Industry in North Macedonia

Case Details

Title: Financial Power of the Macedonian Retail Market

Prepared by: Sergej Zafiroski, General Manager

– Insider ID (Research & Consulting Agency)

Analysis Period: 2019–2025 (with projections)

Scope: Market structure and financial performance of the FMCG sector in North Macedonia, including food, beverages, and tobacco. The analysis covers revenue growth, market share by retail concept (hard discount vs. classic chains), consumer behavior, profitability trends, and competitive dynamics among national and local supermarket chains.

Methodology Note: The analysis is based on officially published statistical data, financial reports of retail chains, and proprietary market research conducted by Insider ID. Turnover, growth rates, and market shares are calculated using standardized indicators to ensure consistency, comparability across years, and alignment with inflation-adjusted market conditions.

Let’s Work Together for Development

Call us directly, submit a sample or email us!

Address Business

Hopkins, Minnesota(MN), 55305

Contact With Us

Herringtonconsulting@gmail.com

Working Time

Holiday : Closed

Navigating the Future: Supply Chain, Digitalization and Consumer Behavior in the FMCG Industry in North Macedonia

Part of the information is derived from the research “Navigating the Future: Supply Chain, Digitalization and Consumer Behavior in the FMCG Industry in S. Macedonia”. The report is part of a larger project implemented by Insider ID, in cooperation with the European Bank for Reconstruction and Development and financial support from the European Union – Enterprise Development and Innovation Fund for the Western Balkans (WB EDIF). The entire report is available on the Insider ID website (www.insider.mk).

When talking about a supply chain, consumers are the last link, i.e. the actual user to whom the final product is delivered and who pays for it. By excluding the consumer, the entire supply chain would not exist at all, because there is no one to exchange money for the final product. Consequently, consumer behavior, their preferences and thinking about the positions of brands are crucial for maintaining the entire system.

Companies often overlook the impact and importance of consumers on the supply chain, seeing them as an element outside of it or just one part of the entire process.

What is the size of the domestic market?

According to the data in the report, there are a total of 1.46 million active consumers (resident population over 18 years of age) who generate a total turnover in the “Food, beverages and tobacco” sector of 1.91 billion euros (source: SSO). The projection is that in 2024, the total market in the same segment will amount to 2.25 billion euros, or approximately an additional 260 million euros will be generated in the current year. Part of that growth will be caused by inflation, i.e. the increase in product prices, but also part due to increased consumption by consumers.

There are 8 national supermarket chains operating on the market, of which three are hard discounts (KAM Market, Kipper and Stokomak) and 5 are classic chains (Tinex, Vero, Ramstore, Kit-Go and Zito Market). In addition, there are more than 25 local chains on the Macedonian market, which are represented in one or several cities.

The total turnover generated by national chains in 2024 is expected to be approximately 1.15 billion euros, of which 713 million would be generated by hard discounts, while the remaining 439 million euros from classic chains. In terms of share, TDs generate 66% of the total turnover of national chains or 33% of the total turnover in the “Food, Beverages and Tobacco” segment.

From a financial perspective, there is sufficient potential for the development not only of existing domestic companies, but also of the introduction of new products that are yet to be placed on the domestic market. The additional 260 million euros for 2024 and the desire of consumers for a greater number of domestic products indicate that there is potential for companies that is currently available.

Digitalization and e-commerce in the FMCG Industry

The main conclusion in this regard is that significant improvement is needed first of all in internal processes, i.e. their digitalization, and then to continue with inter-company connectivity and e-commerce. In fact, in the supply chain there is low integration and connectivity between the companies’ systems, which does not allow for optimization of processes and cost reduction. Such a situation is caused by low innovation of domestic companies and implementation of software solutions that will replace some of the repetitive processes and those segments of operations where automation is possible. Managers state that it is necessary to accelerate the process of digitalization and integration of chains, in order to reduce costs but also to increase the competitiveness of domestic companies on the international market.

E-commerce of consumer goods

E-commerce is undoubtedly the channel that will develop significantly in the next decade on the domestic market. Companies need to adapt internal processes and develop appropriate software solutions to meet future demand. However, currently, according to managers and consumers, the readiness of the domestic market and the number of consumers who would prefer to shop through an e-store is not at the necessary level that will enable economies of scale and a sustainable business model.

According to managers, the five main barriers to the development of consumer e-commerce in Macedonia are the financial size of the market, the available time of consumers, the proximity of markets to the place of residence and work, low trust in the quality of products and low digital readiness of companies.

The results of the consumer survey confirm the managers’ thoughts. Although approximately 15% of consumers have purchased products through an e-store so far, between 2% – 5% prefer to shop online instead of in a classic market. In general, consumers are distrustful of whether the food product they will buy through an e-store will be of high quality (and fresh) and they want to see the product before buying it.

Approximately half of consumers would buy a product from a manufacturer/distributor’s e-store if the price of those products were lower than the market price, which indicates great potential for future development. However, this “direct” way of selling from distributors and manufacturers to end customers has challenges from a logistical (number and physical size of orders) and financial aspect (individual order value), which currently make it impossible to establish a profitable business model.

One of the key e-commerce-related insights from the research is the product categories that consumers would purchase through that channel. Companies that operate in categories with products with a longer shelf life or standardized quality are more likely to use digital channels in the medium term. In fact, what the results indicate is that if consumers were “forced” to buy through an e-store, they would buy products that they are convinced have a longer shelf life and standardized quality. The structure of responses among consumers who have not purchased a product online again indicates a preference for future online purchases of categories with standardized quality and a longer shelf life, while the other categories lag significantly behind.

Marketing and branding of domestic companies

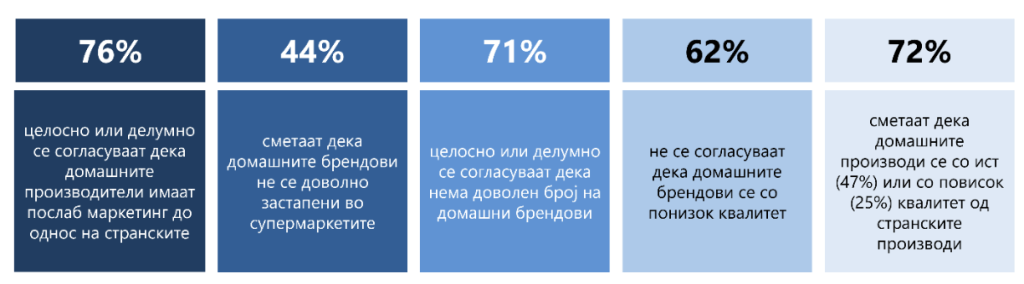

One of the main findings of the research is that there is untapped potential for domestic brands, as both consumers and companies believe that domestic supply should be increased. An additional positive is that a majority of consumers believe that the quality of domestic products is at the same level as foreign ones, but they lack quality marketing and branding to break into the market.

According to the data, 76% of consumers believe that domestic brands have weaker marketing, 72% that domestic products are of the same or higher quality than foreign ones, 71% that there are not enough domestic brands at all that are produced in the country.

The key comment of managers regarding branding and marketing is that companies need to focus on innovation and creating a unique competitive advantage for their brands (and products) that will provide additional value in the category where they are represented. If competition is based only on changes in product characteristics, it will only cause cannibalization of the category, without providing additional value for consumers and all participants in the supply chain.

Next steps

The relationships between participants in the supply chain are significantly complex and consumers are demanding and specific. The domestic market, although small compared to other countries in the region, does not lag behind in terms of the number of participants and the challenges that companies face in meeting the requirements. The stated need for domestic products by consumers and the financial value of the market indicated that there is currently a significant market for new brands and companies. Introducing new and improving the position of existing domestic brands will not only improve the position of the company that owns them, but also the entire supply chain. A larger number of domestic brands also indicates a larger number of manufacturers, suppliers and associated industries that will focus on their successful commercialization. What companies need to focus on in the short and medium term is the complete digitalization of internal operations and integration between company systems. In parallel, they should improve marketing and branding, which on the one hand will improve the perception among domestic consumers, but will also increase the likelihood of success on the international market.